How to Buy UK Property from Abroad

In this guide

Fully remote — no need to fly over

Viewing, offering, signing and submission can be remote; a power of attorney covers final signing. Flying over is preference, not a requirement.

Exchange is not completion

Exchange = legally binding, ~10% deposit paid; completion = balance paid, title transfers, keys handed over — only then is it done. They can be days to weeks apart.

Prepare source-of-funds early

AML needs notarised ID, 6–12 months of statements, a direct transfer with a reference. A parental gift also needs a gift letter. Prepare early to avoid delay.

Non-resident mortgage: use a specialist

High-street banks favour UK income; overseas buyers use a specialist lender or broker and get a mortgage in principle first. Terms vary by individual, so a specialist assesses them case by case.

Take care with off-plan and new builds

Off-plan: watch completion delays and deposit-protection terms; a new build's NHBC warranty is not a survey — arrange a snagging survey at completion.

Work out stamp duty for your situation

Overseas buyers may face surcharges and the rules vary by situation. Use the IREIS calculator for your circumstances and confirm with a solicitor.

For many families and investors looking to the UK, the first — and most off-putting — question is rarely “which flat”, but rather: from overseas, can I actually complete a UK purchase? At what point is the deal really done? And if something goes wrong midway, is my deposit safe?

This guide, from IREIS Properties, sets out the complete buying process in England and Wales for overseas buyers — from financial preparation through to completion, step by step. By the end, you will know what each stage involves, who is helping you, and where to take the most care. Bought with the process understood, an overseas purchase is far steadier and more predictable than it first appears.

Can I complete the whole purchase remotely, without coming to the UK?

Yes. Overseas buyers do not need to live in the UK to buy. Almost every stage can be handled remotely: viewing online, offering through an agent, signing electronically, and having your solicitor submit on your behalf. Two things need careful arrangement. First, identity and source-of-funds verification (see the anti-money-laundering section) requires documents prepared in advance. Second, if you cannot even handle the final signing yourself, a power of attorney lets you appoint someone you trust, or your solicitor, to sign for you. Whether to fly over is a matter of preference, not a legal requirement — many overseas buyers complete from first viewing to collecting the keys without ever setting foot in the UK.

Who you will work with

A UK purchase usually involves several professionals, each with a distinct role. The estate agent acts for the seller. A buying agent works on your side — finding properties and negotiating for you, which is especially valuable for an overseas buyer who cannot easily attend in person. The conveyancing solicitor handles the transfer of title and all the legal paperwork. A chartered surveyor inspects the property’s condition. If you need finance, a mortgage broker experienced with non-resident cases arranges it. And a specialist FX broker helps with cross-border currency exchange. Knowing who does what tells you, at each step, who to turn to and whose job it is to protect your interest — and it is the surest antidote to the feeling that an overseas purchase is somehow opaque.

Step 1: Financial preparation

Before anything else, settle whether you are buying with cash or with a mortgage, as this drives both the timeline and the paperwork. If you need a mortgage, overseas and non-resident buyers should note that most high-street banks favour applicants with UK income; overseas buyers usually arrange finance through a specialist lender or broker experienced with non-resident cases, and obtain a mortgage in principle first. Loan-to-value and terms vary widely by individual — leave this to a specialist to assess case by case — the right number is always the one that fits your own circumstances.

Step 2: Finding and viewing

The main UK property portals are Rightmove and Zoopla; overseas buyers can also shortlist remotely via video viewings, walk-through films and floor plans. But a screen makes it hard to judge light, the floor level, the surroundings and the true condition of a property, so a more reliable approach is to appoint a buying agent familiar with overseas buyers’ needs to vet properties on the ground and filter out unsuitable ones before you waste time on them.

Step 3: Offer and negotiation

Once you have found a property, you offer to the seller through your agent. UK negotiation has its own rhythm and conventions — the level of your offer, how you respond to a counter-offer, and when to hold firm versus when to concede all affect the final price. Once an offer is accepted, a reservation fee is usually paid to secure the property and the legal process formally begins.

Step 4: Appointing a solicitor and source-of-funds verification (AML)

Next, appoint a solicitor (a conveyancer) to handle the transfer of title. Overseas buyers should choose a solicitor experienced with remote and cross-border cases, who will be more familiar with remote identity checks (KYC) and with overseas funds.

Under the UK’s anti-money-laundering rules, your solicitor must verify the lawful source of your funds. Overseas buyers should prepare early: notarised proof of identity, bank statements for the past 6 to 12 months, and a clear money trail (a direct transfer from your own account with a clear reference). If the funds come from a parental gift, the documentary requirements are more detailed — we cover this fully in our complete guide to buying UK property for your children. Allow plenty of time so that verification does not hold up the overall progress.

Step 5: The core legal process — from accepted offer to completion

This is the backbone of the whole process, and you must understand the difference between the key milestones:

- Offer accepted — the seller agrees verbally, but there is no legal commitment yet; either party can still withdraw.

- Conveyancing and searches — your solicitor carries out local authority, environmental and drainage searches to confirm the title is clean.

- Exchange of contracts — both sides formally sign and exchange contracts. From this moment the transaction is legally binding, and a deposit of around ten per cent is usually paid at the same time; backing out afterwards risks losing that deposit.

- Completion — the balance is paid, title transfers into your name, and you receive the keys. Only now is the deal truly done.

In short: exchange is the “binding”, completion is the “done”. The two can be days to weeks apart. If one party fails to complete after exchange, the other can serve a “notice to complete” requiring performance within a set period. For this reason, if you are buying with a mortgage, watch the validity period of your mortgage offer carefully — do not let it expire before completion, or you may have to re-apply at the worst possible moment.

Step 6: Survey

Appoint a chartered surveyor to inspect the property and understand its structure and any underlying issues. A common misconception is that “a new build has an NHBC warranty, so no survey is needed” — they are not the same: a warranty is not the same as someone checking the workmanship now. On a new build, you can arrange a snagging survey at completion to list defects for the developer to remedy before handover.

Buying off-plan: special considerations

Buying a property not yet built carries its own timeline and risks: completion may be delayed, and you should understand exactly what protects your deposit and what happens if the developer runs into financial difficulty. Before committing, have your solicitor scrutinise the contract terms on the completion longstop and on deposit protection, and be clear that phased schemes complete in stages, building by building. For an off-plan buyer, caution is your best friend.

How long does it take, from offer to keys?

There is no fixed timetable. From an accepted offer to completion can take anywhere from several weeks to a few months, depending on the conveyancing searches, whether a mortgage is involved, whether the property is off-plan (where you may be waiting for construction to finish), and the length of any chain. Cross-border cases add some time for document exchange and verification — this is within the normal range, not a red flag. The two things most within your control are appointing an experienced solicitor early and having your source-of-funds documents ready before they are asked for.

Transferring funds and currency exchange

Completion requires the balance to be ready in the UK. Cross-border purchases inevitably involve currency exchange, and the timing and cost of that exchange are a commercial decision, not a bet that can be predicted. Our advice is consistent: consult a specialist FX broker to monitor the rate and, where possible, lock in a forward contract ahead of completion to manage the cost of exchange. A regulated FX provider is often cheaper than an ordinary bank — and keep every exchange receipt as part of your source-of-funds file.

Stamp duty and other costs

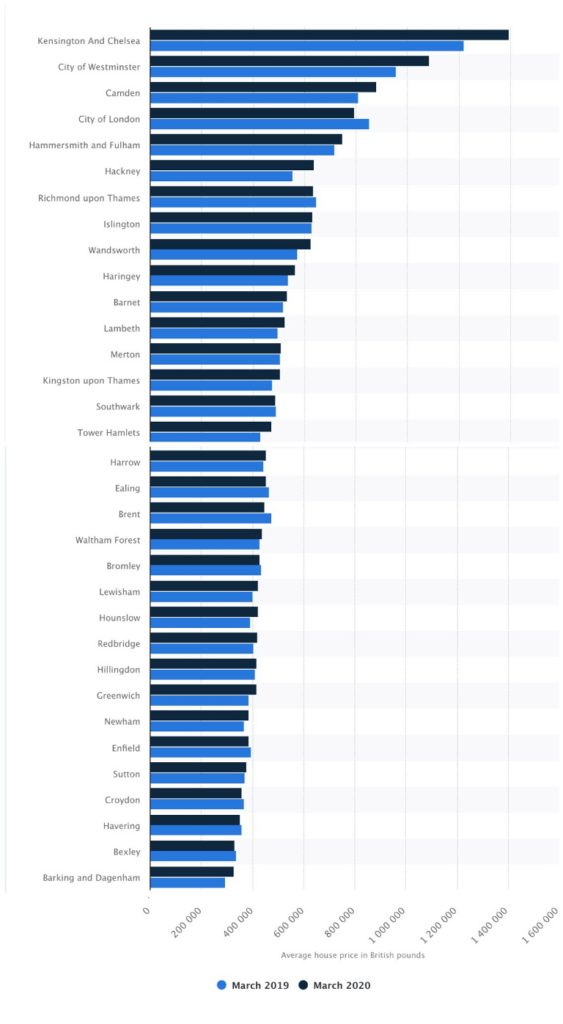

The cost of buying is not only the price. Beyond stamp duty there are legal fees, land registry fees, valuation fees, telegraphic transfer fees, and the survey and currency costs noted above — all of which belong in your budget. Stamp Duty Land Tax in particular is complex in structure, and overseas buyers may face surcharges, so the surest route to a precise figure is our UK Stamp Duty Calculator for your own circumstances — then have your solicitor confirm.

In closing: understood, an overseas purchase is far from daunting

The UK buying process has many stages, but each has a clear role and meaning. Understood, an overseas, remote purchase is steady and predictable. The London-based, tri-lingual advisory team at IREIS Properties can guide you at every step and introduce solicitors, mortgage specialists and FX professionals experienced with overseas cases. For more context, see our Buying Guides and Tax & Legal sections. And to get the tenure terms clear first, see UK property tenure explained. To get all the costs and taxes in one place, see our UK property costs and taxes overview.

Frequently asked questions

Can I complete the whole purchase from overseas without coming to the UK?

Yes, and you need not fly over. Viewing, offering, signing and submission can largely be done remotely; if you cannot handle the final signing yourself, a power of attorney lets someone you trust, or your solicitor, sign for you. Flying over is a preference, not a legal requirement.

What is the difference between exchange of contracts and completion?

Exchange of contracts is the moment the transaction becomes legally binding — a deposit of around ten per cent is usually paid then, and backing out afterwards risks losing it. Completion is when the balance is paid, title transfers and you get the keys — only then is the deal done. The two can be days to weeks apart.

What ID and documents do overseas buyers need?

Under anti-money-laundering rules, typically notarised proof of identity, bank statements for the past 6 to 12 months, and a clear, traceable money trail (a direct transfer from your own account with a reference). If funds are a parental gift, a gift letter and further documents are also needed. Prepare early.

How long does it take from offer to keys?

It varies — there is no fixed number of days, but typically several weeks to a few months. It depends on conveyancing searches, mortgage approval, whether it is off-plan, and the complexity of the chain. Appointing a solicitor experienced with overseas cases and preparing source-of-funds documents early are the keys to a smooth timeline.

When is the ten per cent deposit paid, and when the balance?

The deposit of around ten per cent is usually paid at exchange of contracts; the balance is paid at completion, when title transfers and you receive the keys. The exact amounts and timing are set by the contract — have your solicitor confirm each item.

What are the risks of buying off-plan, and is my deposit protected?

The main risks are completion delays and the developer's financial position. Before committing, have your solicitor scrutinise the contract's completion longstop and deposit-protection terms and clarify exactly what protects your deposit. Careful review of the contract is an off-plan buyer's most important safeguard.

Do I still need a survey on a new build — isn't the NHBC warranty enough?

A warranty is not a survey. An NHBC-type warranty is not the same as someone checking the current workmanship. On a new build you can arrange a snagging survey at completion to list defects for the developer to remedy before handover.

Why is conveyancing so slow, and what is a 'notice to complete'?

Conveyancing (searches and verification) takes time, and cross-border document exchange lengthens it — this is within the normal range. If a party fails to complete after exchange, the other can serve a 'notice to complete' requiring performance within a set period, failing which there are consequences for breach.

Can overseas buyers get a UK mortgage?

Yes, but most high-street banks favour applicants with UK income, so overseas and non-resident buyers usually arrange finance through a specialist lender or broker experienced with non-resident cases. Loan-to-value and terms vary by individual, so leave it to a specialist to assess case by case.

Featured developments

Prefer to see them in person? Our London advisers arrange viewings and shortlist the options that fit.

The Forge

A considered collection in South London, from £199,950

Brindley Collection

Canal-side architecture in Birmingham's Learning Quarter — HS2-ready, Glenn Howells-designed, from £232,500

Urban Picturehouse

Art Deco heritage meets contemporary living on the doorstep of Southeastern rail

London-based, trilingual UK property advisers for overseas and domestic buyers. Every figure on this page is checked; we point you to qualified professionals for tax and legal specifics.

Talk to an IREIS adviser

Tell us your budget, area and plans — we’ll introduce the options that fit, without the hard sell.

On desktop? Scan with your phone to start the conversation.